In college, my minor was psychology. My thesis was on heuristics, cognitive biases, and the decision-making process. I have always been fascinated by the way the mind works.

Nobel Laureate Daniel Kahneman’s best seller, “Thinking Fast and Slow,” offers a valuable insight into how we make decisions. Click here to view a 2-minute analysis of Kahneman’s thoughts.

When I created the Active Management Value Ratio™ (AMVR) metric, it was based on these same principles. The goal was to provide a metric that could help investors, including plan participants, make meaningful investment decisions.

Based on my 30+ years in the investment industry, initially as a securities compliance director for both broker-dealers and registered investment advisers, and now as a securities and ERISA attorney and consultant, I believe that the two primary reasons some investors make poor investment decisions is a lack of information/education, and misplaced reliance on illusory investment returns and investment advice.

Psychology and Decision-Making

The reference to investment “illusion” refers to various misconceptions about investment returns and investment advice. In many cases, those misconceptions are the result of the influence of psychological heuristics and cognitive biases.

Heuristics are mental shortcuts that people take in making decisions. The bat/paddle and ball analogy in the Kahneman video is an excellent example of how we use heuristics to simplify the decision-making process, the intuitive or “fact thinking” process.

The problem that a decision-maker must consider is that heuristics can often result in errors due to the influence of cognitive biases that may influence a decision-maker’s judgment. Common cognitive biases that influence decisions include

- Confirmation bias – the tendency to give greater weight to information that confirms our existing beliefs.

- Anchoring bias – the tendency to put greater emphasis on and credibility to the first piece of information that we hear.

- Authority bias – the tendency to blindly rely on any and all advice and recommendations provide by those appearing to have expertise on a topic.

- “Halo effect” – the tendency for an initial impression of a person to influence the overall and ongoing opinion we have of them.

Based on my experience, these four cognitive biases often come into play in the investment decision-making process. In my opinion, the most damaging example of this problem is the authority bias. Far too often, investors blindly rely on investment advice and recommendations that they believe are objective and in their best interest, from a “trusted adviser,” someone they believe is far more experienced and knowledgeable in such matters. Unfortunately, in far too many cases, the reality in many cases is that the “trusted adviser” is simply someone simply trying to sell an investment product, or as one expert said, “someone whose job it is to make money on you, not for you.”

Psychology and the Active Management Value Ratio™

As I mentioned, heuristics and cognitive biases were a primary consideration when I created the AMVR metric. As the video points out, the influence of large numbers is a well-known cognitive bias.

What would be your initial reaction if I were to recommend this investment to you?

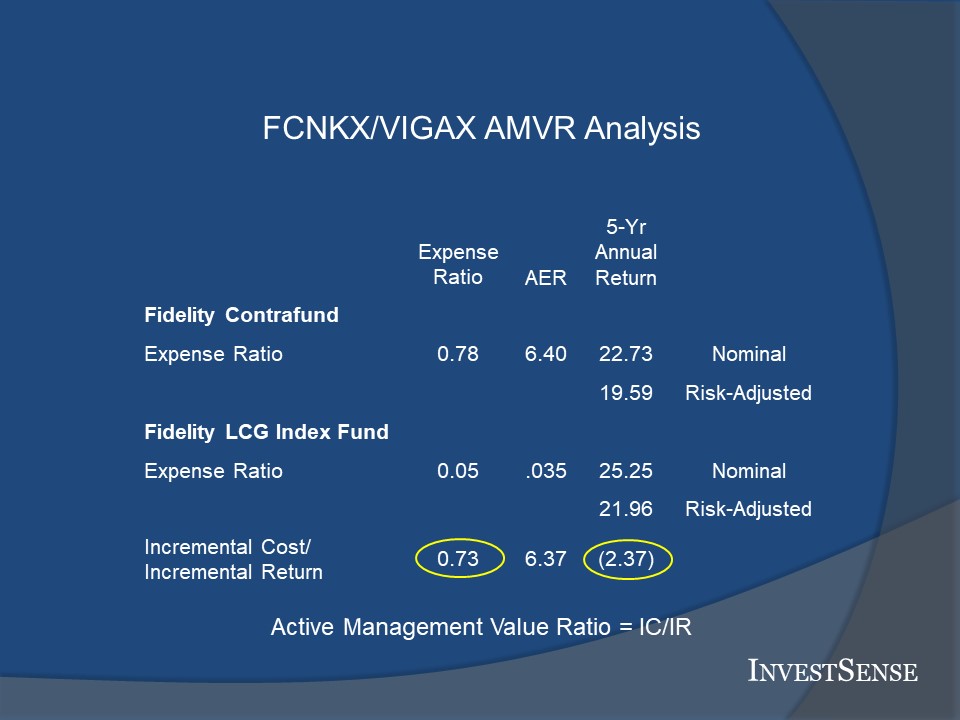

In many cases, the intuitive/fast thinking model would notice the 22.73 percent return with an expense ratio of “only” 78 basis points. 22.73 vs. 0.78. The initial intuitive reaction would most likely be very positive.

Now, what would be your reaction if you were presented with the following AMVR forensic analysis slide on the same investment?

Hopefully, an investor’s rational, “slow thinking” decision-making side would quickly convince them that the is not be the “bargain” it first appeared to be relative to a comparable index fund. This opinion is supported by the opportunity to consider the two investments based on a cost-efficiency comparison.

The actively managed fund not only failed to provide a positive benefit, or incremental return, but also had a significant incremental cost. Costs matter. A simple rule of thumb for investors to remember is that over a twenty-year period, each additional 1 percent in investment costs/fees reduces an investor’s end-return by approximately 17 percent.

The Illusion of Investment Returns

While the “illusion” of investment returns refers to the errors in judgment resulting from issues with heuristics and cognitive biases, it also refers to errors in evaluating investments due to the failure to properly assess the effective costs of actively managed mutual funds.

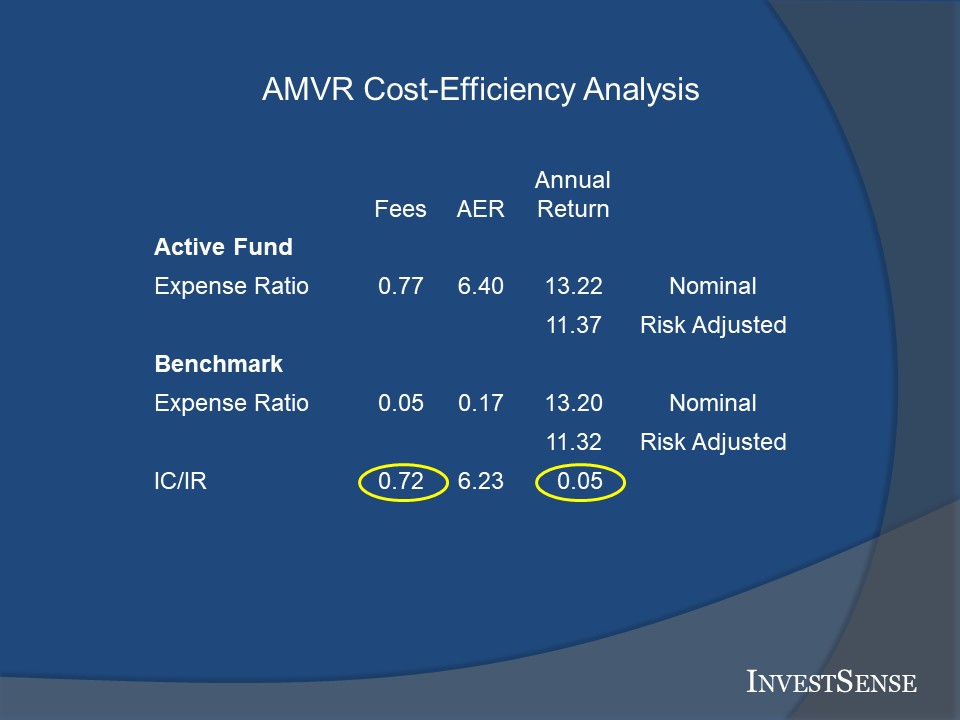

The chart above shows cost-efficiency in terms of a fundamental cost/benefit analysis, incremental costs relative to incremental returns. The actively managed fund failed to produce a positive incremental return. As a result, the prudence analysis was easy.

A common error in evaluation occurs when the actively managed fund does provide a positive incremental return. The AMVR analysis below shows such a situation.

The chart is significant in two ways. First, it shows that an investor could achieve approximately 99.5 percent of the actively managed fund’s return at a much lower cost, 5 basis points. A basis point equals .01 percent of 1 percent; 100 basis points equals 1 percent.

Second, that means that we are effectively paying 72 basis points, the incremental cost, for just 5 additional basis points of return, the incremental return. Paying a cost/fee fourteen times the benefit/return received is obviously an issue in terms of prudent investing.

Advanced Cost-Efficiency

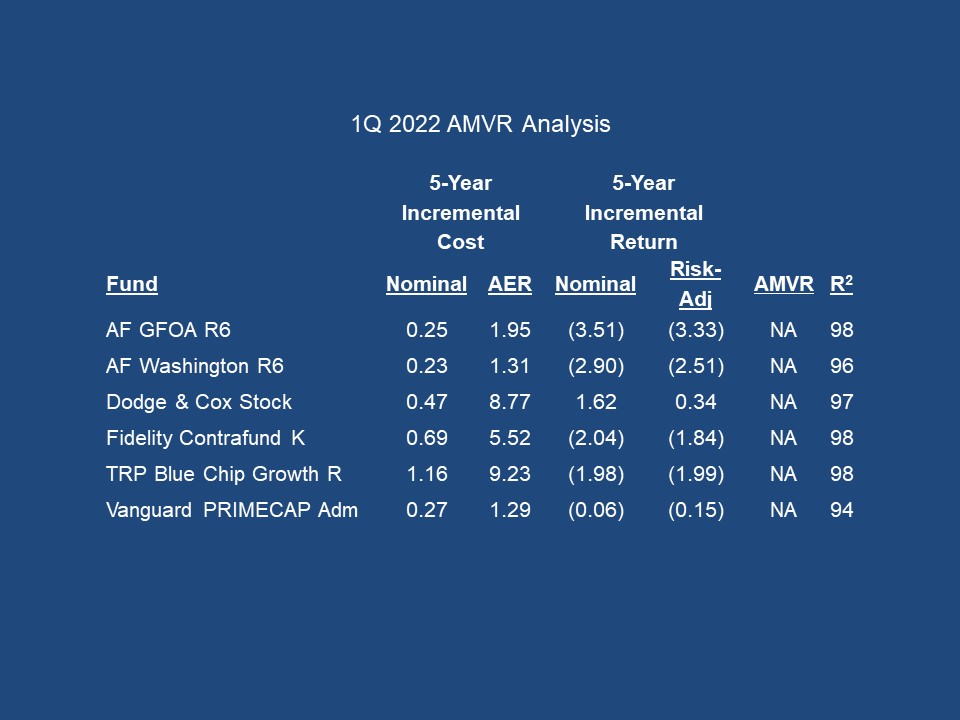

At the end of each calendar quarter, I prepare an AMVR “cheat sheet” for my investment fiduciary consulting clients, such as pension plan sponsors and trustees. The “cheat sheet” for the first quarter of 2022, for six of the most popular investment options in U.S. defined contribution plans, e.g., 401(k) plans, is shown below.

I provide two sets of data, one based on the funds’ publicly stated, or nominal, information, the second based on incremental risk-adjusted returns and incremental correlation-adjusted costs. For more information about why I provide the adjusted returns and costs, click here.

Comparing the funds on a nominal cost/nominal return basis, five of the six funds failed to even outperform the comparable index fund, making them an imprudent investment choice. The fact that they paid additional costs for such underperformance only makes matters worse. One fund, Dodge & Cox Stock would have been cost-efficient, as its nominal incremental return (1.62) exceeded it nominal incremental cost (0.47).

Comparing the funds on an adjusted cost/adjusted return basis results in the similar scenario, with the same five funds still proving to be imprudent investment choices. However, using the adjusted numbers, Dodge & Cox Stock also proves to be an imprudent investment choice, as its incremental correlation-adjusted cost (8.77) significantly exceeds its incremental risk-adjusted return (0.34).

The Dodge & Cox Stock scenario provides a perfect example of why investors should consider risk-adjusted returns and correlation-adjusted costs in making investment decision. Dodge & Cox’ Stock’s relatively high expense ratio combined with its high r-squared, or correlation, number to drive up its effective expense ratio. Invest Sense calculates a fund’s incremental correlation-adjusted cost using Miller’s Active Expense Ratio.

Many online investment sites include a fund’s r-squared number. Investors considering actively managed mutual funds should always note a fund’s r-squared number for two reasons. First, it helps warn investors about potential “closet index” funds. Closet index funds are funds that tout the advantages of active management, but in reality provide end-returns similar to, in many cases worse, than the end-returns of comparable, but less costly, index funds.

Second, a fund’s r-squared number indicates the likelihood that an actively managed fund will be able to outperform a comparable index fund. Actively managed funds operate at an inherent disadvantage to index funds due to their higher fees and expenses, e.g., management fees and trading costs. A high r-squared number means that the actively managed fund closely mirrors the performance of a comparable index or index fund, making it unlikely that the actively managed fund will be able to make up for such higher expenses.

Going Forward

People often indicate that they are confused and intimidated by the investment process. That was another reason that I created the Active Management Value Ratio™ metric and made it as simple as possible. While many investors focus only on returns, returns without accompanying cost-efficiency are essentially meaningless, as it indicates that an investment’s incremental investment costs exceed its incremental investment returns. Cost exceeding returns is never a sound investment strategy.

The information needed to perform an AMVR analysis on a nominal basis is freely available online. The AMVR “cheat sheet” analysis showed that in many cases, an AMVR analysis based on a fund’s nominal costs and returns alone is enough to expose cost-inefficient mutual funds.

Investors willing to go online, find the cost and return information, and perform what one judge described as “third grade math” can easily calculate the cost-efficiency of their existing and prospective investments and hopefully improve their investment success and financial security.