James W. Watkins, III, J.D., CFP EmeritusTM, AWMA®

Investors often suffer unnecessary investment losses due to lack of accurate information and/or misperceptions about investment markets, improper investment products, and the quality of advice provided by investment professionals. The InvestSense Challenge was created to increase investor awareness of some of the leading reasons that investors suffer such losses and to suggest strategies and techniques that investors can use to protect against such losses.

1. True or false?

Stockbrokers, investment advisers, and other financial consultants are required to always put their customers’ interests ahead of their own and to fully and completely disclose any actual or potential conflicts of interest.

2. Which of the following statements is true about variable annuities?

A. If you annuitize a variable annuity in order to receive a lifetime stream of income, you must give up ownership of the annuity and the money in the annuity and, upon your death, the insurance company that issued the variable annuity, not your heirs, receives the balance in the annuity.

B. Variable annuity issuers often base their annual fee for the guaranteed death benefit on the accumulated value of the variable annuity, even though the guaranteed death benefit provision in most variable annuities only obligates the issuer to repay the annuity owner’s designated beneficiaries an amount equal to the owner’s actual capital contributions.

A. Only Statement A

B. Only Statement B

C. Both Statements A & B

3. The projected return/risk profile of your actual investment portfolio is

A. annual return less than 12%, annual standard deviation greater than 12%.

B. annual return greater than 12%, annual standard deviation less than 12%.

C. annual return and annual standard deviation both greater than 12%.

D. not reliable.

4. True or false?

Asset allocation explains 93.6% of the investment returns of an investment portfolio.

5. True or false?

A ‘break-even” analysis allows an investor to compare the effect of fees and other costs on available investments.

6. According to the Department of Labor and the General Accountability Office, each additional 1 percent of fees/costs reduces an investor’s end-return by approximately ____ over a twenty year period.

A. 9%

B. 12%

C. 17%

D. 20%

7. True or false?

“Closet index funds” are mutual funds that tout the benefits of active management and charge higher fees accordingly, yet consistently produce returns that are similar to, in many cases less than, the returns of comparable index funds.

8. According to investment experts such as Charles Ellis, William Sharpe, and Burton Malkiel, the most valuable factors to consider in evaluating an actively managed mutual fund include all of the following factors except:

1. Features of comparable index funds.

2. The cost-efficiency, the costs relative to the returns, of a fund

3. A fund’s expense ratio and trading costs.

Answers

1. True or false?

Stockbrokers, investment advisers and other financial consultants are required to always put their customers’ interests ahead of their own and to disclose fully and completely any actual or potential conflicts of interest.

Investment advisors, including financial planners, are, by law, fiduciaries. As fiduciaries, they are held to the highest standards in connection with their dealings with the public. Fiduciaries are required to always put their clients’ interests first and to disclose any actual or potential conflicts of interest.

Depending on the circumstances, stockbrokers may not considered to be fiduciaries. Consequently, they may not be required to put their clients’ interests first, or to disclose all information regarding actual or potential conflicts of interest. While fiduciaries are required to only recommend investments that are legally prudent and in a client’s best interests, stockbrokers are regulated under a different standard of care,

The Securities and Exchange Commission recently enacted a regulation known as Regulation Best Interest.” (Reg BI). On its face, Reg BI holds stockbrokers to the same standards of conduct and disclosure requirements that are requiored of investment fiduciaries. However, there are still questions as to the effectiveness of Reg BI in terms of investor protection. These questions are due primarily to the fact that Reg BI does not define what is required under either the “best interest” standard. Furthermore, Reg BI’s “reasonably available alternatives” clause arguably provides a loophole for stockbrokers, by which broker-dealers and stockbroker can continue to put their bests interests ahead of those of a customer.

2. Which of the following statements is true about variable annuities?

A. If you annuitize a variable annuity in order to receive a lifetime stream of income, you must give up ownership of the annuity and the money in the annuity and, upon your death, the insurance company that issued the variable annuity, not your heirs, receives the balance in the annuity.

B. Variable annuity issuers often base their annual fee for the guaranteed death benefit on the accumulated value of the variable annuity, even though the guaranteed death benefit provision in most variable annuities only obligates the issuer to repay the annuity owner’s designated beneficiaries an amount equal to the owner’s actual capital contributions.

A. Only Statement A

B. Only Statement B

C. Both Statements A & B

Assuming that an annuity owner annuitizes the variable annuity and the “single life” option is chosen, upon the owner’s death, the life insurance company that issued the variable annuity, not the owner’s designated beneficiaries, will receive the balance remaining in your annuity. If the “joint survivor” option or the “last to die option” is chosen, the insurance company will receive the balance remaining in the annuity, if any, upon the second person’s death. This inability to pass one’s life savings on to their heirs is one of the primary reasons that many financial advisors caution their clients not to purchase variable annuities.

Variable annuity salesmen also tout the guaranteed death benefit (“GDB”) offered by variable annuities. In most cases, the GDB only guarantees that if the annuity owner dies without annuitizing the annuity and the value of the annuity is less than the owner’s actual capital contributions, the insurance company will pay the variable annuity owner’s designated beneficiaries an amount equal to the annuity owner’s actual capital contributions.

While the actual value of a GDB is questionable for long term investors given the historical performance of the markets, the cost of a GDB is even more questionable given the fact that most insurance companies calculate the cost for the variable annuity’s GDB on the accumulated value of the variable annuity rather than on the amount they are legally obligated to pay under the GDB, which is often significantly less the variable annuity’s accumulated value.

For example, if you invest $100,000 in a variable annuity, and the value of the annuity grows to $250,000, the insurance company that issued the annuity may charge you an annual fee for the GDB based on $250,000, even though they are only liable for paying $100,000. When you consider that the fee for the GDB is usually a variable annuity’s largest annual fee, often in the range of 1.5% to 2% of the value of the variable annuity, and multiply that over a number of years, you can understand how profitable this can become for the annuity issuer andabusive this can become for the annuity owner.

Variable annuities may make sense for a limited few. However, for many investors, the high fees and expenses, the tax issues, and the potential loss of substantial assets to leave to one’s heirs make a variable annuity an unsuitable investment.

For more information about the various issues regarding variable annuities, click here to read our white paper, “Variable Annuities: Reading Between the Marketing Lines.”

3. The projected return/risk profile of your actual investment portfolio is

A. annual return less than 12%, annual standard deviation greater than 12%.

B. annual return greater than 12%, annual standard deviation less than 12%.

C. annual return and annual standard deviation both greater than 12%.

D. not reliable.

For most investors, the correct answer is “D,” especially for those investors who have actually had an asset allocation/portfolio optimization plan prepared.

Financial advisors often prepare asset allocation/portfolio optimization plans for investors. These plans often include recommendations to help the investor “optimize” their investment portfolios to potentially earn greater returns with less risk. Charges for these plans can be substantial, in some cases thousands of dollars.

Unfortunately, the value of such investment advice and performance projections are questionable at best. Some of the most common criticisms of such plans are that

- The projections are usually based on the historical performances of various asset classes, even though “past performance does not guarantee future returns.”

- Some asset allocation plans are based on “guesstimates” of future performance of the investment markets and the economy.

- Most plans and their recommendations/projections are based on broad, generic asset categories rather than an investor’s actual investments;

- The process and the software used to generate such recommendations/projections are inherently unstable and can be easily manipulated to produce desired results.

The questions surrounding some current asset allocation practices have led Dr. William F. Sharpe, a Nobel laureate for his work in the area of portfolio management, to refer to the current situation as “financial planning in fantasyland.”1 The truth is that in too many cases, asset allocation plans are simply a marketing tool to facilitate product sales for financial service companies and financial advisors, with little or no regard for the genuine value provided by such plans. For these reasons, some critics have referred to such asset allocation plans as nothing more than expensive origami and paper airplane kits.

If you have already had an asset allocation/portfolio optimization plan prepared, go back to the financial advisor who prepared the plan and ask them if they ran a similar plan based upon the investments that they recommended or actually sold to you. If they say they did prepare such a plan, ask for a copy of the plan and the return, risk and correlation assumptions that were used to prepare the plan.

1. W. Sharpe, “Financial Planning in Fantasyland,” available on the Internet at http://www.stanford.edu/ ~wfsharpe/art/ fantasy/ fantasy.htm.

4. True or false?

Asset allocation explains 93.6% of the investment returns of an investment

Many investors have heard or read this statement so many times that they simply believe that it has to be true. Truth is, the statement is a misrepresentation, either intentional or unintentional, of what was actually said.

The statement is based on a 1986 study that concluded that asset allocation “explained, on average, 93.6% of the total variation in actual plan returns.” (emphasis added). The main thing that investors need to know about the study is that it analyzed the determinants of the variation of returns, not the determinants of the total returns themselves. Variability of returns is significantly different from total returns, with no absolute correlation between the two.

The authors of the study never claim to have examined the impact of asset allocation on determining actual portfolio returns, let alone claim that asset allocation explains 93.6% of a portfolio’s actual returns. The investment industry, however, has manipulated the findings of the BHB study and combined it with yet another investment myth to promote perhaps the most devastating investment myth of all, the buy-and-hold investment myth. The important point for investors to remember is that asset allocation is an important aspect of the wealth management process, although only one aspect of the process.

5. True or false?

A ‘break-even” analysis allows an investor to compare the effect of fees and taxes on investments options.

In choosing between investment options, investors often fail to factor in the impact of taxes and any fees that an investment may assess. A break-even analysis lets an investor know at what point two investments would provide equivalent after-fees, after-tax returns.

The value of a properly prepared break-even analysis cannot be overstated in terms of investor protection. For example, if you have already purchased an annuity or are considering purchasing one, the annuity salesperson may not have explained the break-even issue with you for your particular purchase or even prepared a written break-even analysis for you, so you knew all about the impact of fees and taxes, right?

Unlikely, as transparency and meaningful disclosure are the financial services and annuity industries’ kryptonite. The typical break-even analysis, when done properly, often reveals both unfavorable aspects of an annuity and the rationale behind the annuity industry well-known saying – “annuities are sold, not purchased.”

Bottom line -whether the proposed investment is an annuity or an actively managed mutual fund, always insist that the broker/agent provide you with a written break-even analysis in case questions arise about the quality of recommendations/advice provided.

For more information about the various issues regarding variable annuities, please read the article, “Variable Annuities: Both Sides of the Story,” on our web site.

6. According to the Department of Labor and the General Accountability Office, each additional 1 percent of fees/costs reduces an investor’s end-return by approximately ____ over a twenty year period.

A. 9%

B. 12%

C. 17%

D. 20%

7. True or false?

“Closet index funds” are mutual funds that tout the benefits of active management and charge higher accordingly, yet such funds consistently produce returns that are similar to, in many cases less than, the returns of comparable index funds.

A mutual fund with a high r-squared number is often a sign of a possible closet index fund. R-squared is a metric that reveals the correlation of returns between two investments or an investment and a market index. So why is there so much discussion and concern internationally over closet indexing? Martijn Cremers, co-creator of the Active Share metric, explains the reason for such concern:

[A] large number of funds that purposrt to offer active management and charge fees accordingly, in fact persistently hold portfolios that substantially overlap with market indices….Investors in a closet index fund are harmed by paying fees for active management that they do not receive or receive only partially….

So should U.S. investors be concerned about possible closet-indexers? Most U.S. domestic equity-based funds are reporting r-squared of 90 or above, with many of the best-known funds reporting r-squared number of 95 and above. These high r-squared numbers should serve as potential indicators of lower effective returns due to closet indexing.

8. According to investment experts such as Charles Ellis, William Sharpe, and Burton Malkiel, the most valuable factors to consider in evaluating an actively managed mutual fund include all of the following factors except:

1. Features of comparable index funds.

2. A fund’s cost-efficiency, a fund’s costs realtive to the fund’s returns.

3. A fund’s expense ratio and trading costs.

4. A fund’s past performance

{T]he best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.7

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!2

Past performance is not helpful in predicting future returns. The two variables that do the best job in predicting future performance [of mutual funds] are expense ratios and turnover.3

One of Wall Street’s best kept secrets is that few actively managed mutual funds are cost-efficient when compared to comparable index funds.

Research has consistently shown that the overwhelming majority of actively managed funds are cost-inefficient.

99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.4

[T]here is Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.5

There is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.6

[T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.7

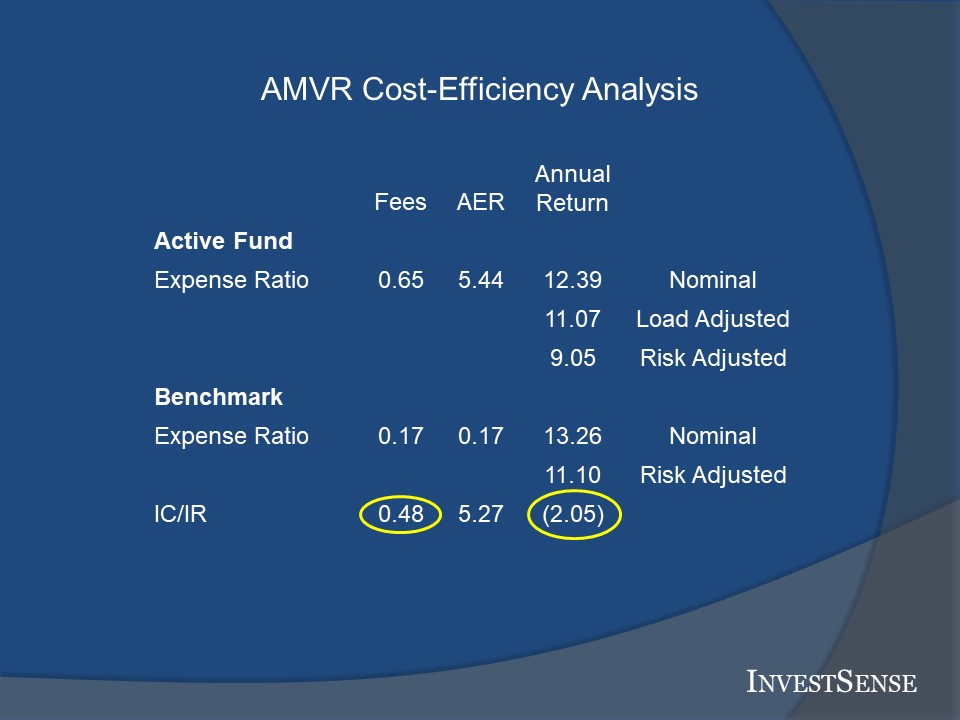

I created a metric, the Actively Management Value RatioTM (AMVR). The AMVR is based on the research and concepts of Ellis, Sharpe, and Malkiel. A sample of an AMVR forensic analysis is shown below.

The example shown is an AMVR forensic analysis of the retail shares of a popular mutual fund. Based upon the combination of the opportunity cost of the fund’s relative underperformance and the fund’s excess cost, the projected loss in end-return for an investor in the fund would be approximately 43 percent5 o er a twenty year period

The cost-inefficiency in the example is even more serious if measured using the AER. In this case, the high incremental costs of the funds combined with the fund’s high correlation of return to the benchmark (98) results in an AER of 5.44.

Retirement shares of actively managed mutual funds commonly used in 401(k) and 403(b) plans are commonly referred to as R-shares or K-shares. The AMVR forensic process used in analyzing the cost-efficiency of retirement shares is essentially the same process as used in analyzing retail shares, with one important difference.

Actively managed retail mutual funds usually charge an investor a “load” to cover the commission paid to the broker who recommended the fund to the customer. The load can either be an immediate, aka “front-end” load, occuring at the time of the initial investment, or a contingent, aka “back-end load, which is only assessed against an investor in the event the investor tries to redeem their shares prior to the passage of a designated period of time. Front-end loads effectively reduce the amount of an investor’s initial investment and, therefore, the investor’s realized returns.

Mutual funds do not charge loads on the retirement shares of their funds. That is why there is no load adjustment to the returns on AMVR forensic analysis of retirement shares.

For additional information on the AMVR metric and the calculation process involved, click the following link.

1. William F. Sharpe, “The Arithmetic of Active Investing.” https://web.stanford.edu/~wfsharpe/art/active/active.htm.

2. Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines.” https://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c

3. Burton G. Malkiel, “A Random Walk Down Wall Street,” 11th Ed., (W.W. Norton & Co., 2016), 460.

4. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010).

5. Charles D. Ellis, The Death of Active Investing, Financial Times,January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e.

6. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016.

7. Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE, 52, 57-8 (1997).

Copyright InvestSense, LLC 2009-2024. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.