Section 7 of the Uniform Prudent Investors Act (UPIA) states that “[w]asting beneficiaries’ money is imprudent.” While the UPIA is directed at trustees and the management of trust assets, common sense tells you that the warning is equally applicable to wealth management in general.

Cost-efficiency is a topic that financial advisers and wealth managers try to avoid. Why?Most studies have consistently concluded that the overwhelming majority of actively managed mutual funds are not cost-efficient, with findings such as

- 99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.1

- Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.2

- [T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.3

- [T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.4

The late John Bogle, founder of the Vanguard Group, often talked about the importance of investment costs and their impact on investor returns. His “Costs Matter Hypothesis” also addressed the fact that just as returns compound, so do investment costs.

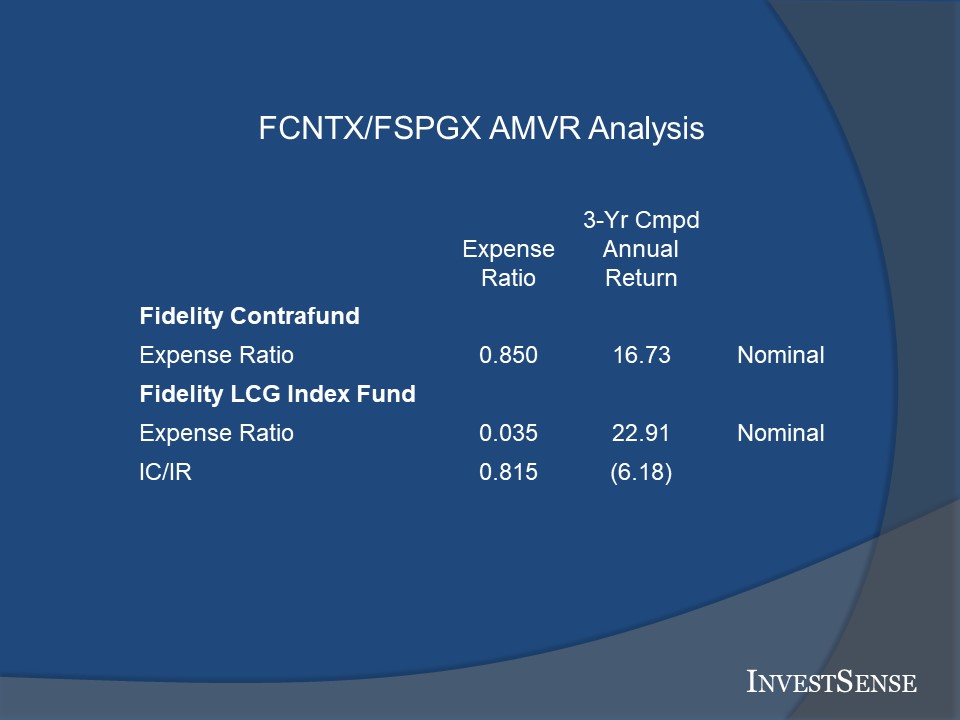

The image below is an example of the forensic analyses we provide to investors, investment fiduciaries and attorneys using our proprietary metric, the Active Management Value Ratio 3.0TM (AMVR). The AMVR allows investors, investment fiduciaries and attorneys to quickly determine the cost-efficiency of an actively managed mutual fund relative to a comparable, but less expensive, index fund.

The chart is an analysis of the retail shares of one of Fidelity’s most well-known and popular mutual funds, Fidelity Contrafund (FCNTX). Will Danoff, the fund’s managers for over 30 years, is one of the most well-known and well-respected mutual fund managers in the industry. However, as the chart shows, the extra costs associated with active management and the fund’s high annual expense ratio result in the fund being cost-inefficient relative to the less expensive Fidelity Large Cap Growth Index Fund (FSPGX).

The bottom line reflects the cost/benefit analysis, or cost-efficiency, of Contrafund in this example. The returns shown here are expressed in basis points, a term commonly used in the investment industry. A basis point is equal to .01 percent of one percent. Therefore, 100 basis point equals one percent. An analogy I often use to help investors understand the importance of the AMVR is to “monetize” the results by asking the following question-“Would you pay $80 to receive only $4 in return?”

The AMVR is simply a version of the familiar cost/benefit methodology. AMVR is simply a fund’s incremental costs (IC) divided by the fund’s incremental return (IR). If a fund’s AMVR is greater than 1.0, it indicates that the fund is not cost-efficient, as its incremental costs are greater than its incremental returns/benefits.

One of the strengths of the AMVR is its simplicity. Once a fund’s AMVR has been calculated the user only has to answer two questions:

- Did the actively managed fund provide a positive incremental return relative to the benchmark?

- If so, did the actively managed fund’s positive incremental return exceed the fund’s incremental costs?

If the answer to either question is “no,” then the actively managed fund does not meet the standards of cost-efficiency set out in the Restatement (Third) of Trusts’ fiduciary standards. Here, Contrafund’s retail shares would be deeded inefficient under the Restatement’s prudence standards, as the fund’s failed both questions.

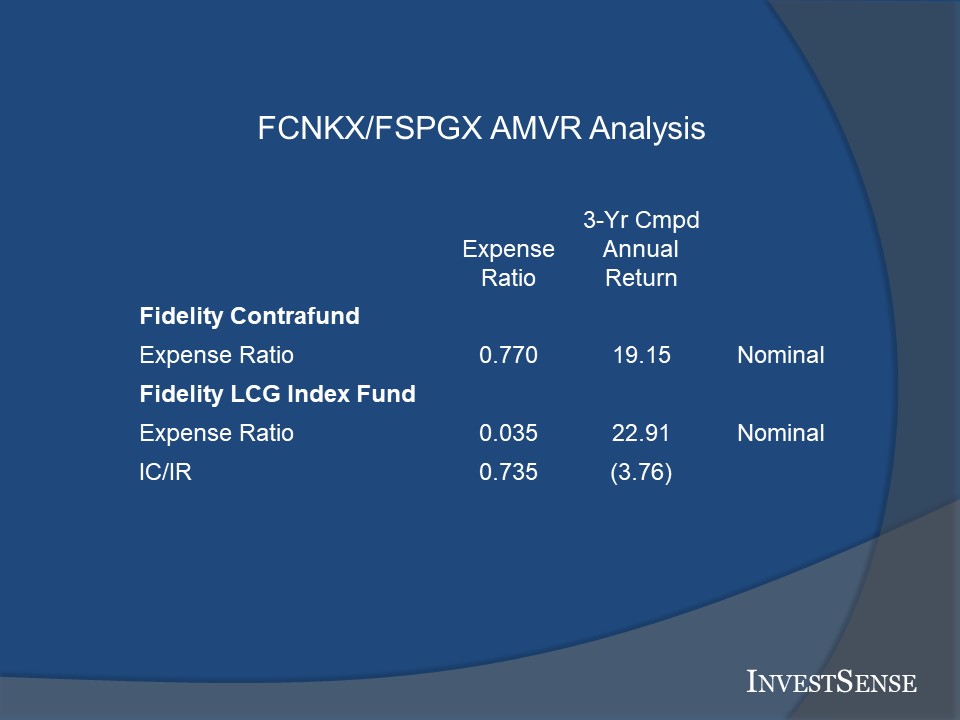

Fidelity Contrafund also offers another class of shares, K shares, that are often offered within 401(k) and 403(b) pension plans. The chart below shows the results of a forensic analysis comparing Contrafund’s K shares (FCNKX) and the Fidelity Large Cap Growth Index Fund.

While the K shares data does change, the results do not. Contrafund’s K shares would be deeded inefficient under the Restatement’s prudence standards, as the fund fails to provide a positive incremental return. Furthermore, the fund’s AMVR score of exceeds the AMVR’s 1.0 guideline.

The purpose of this post was not/is not to point solely to Contrafund’s issues. Trust me, they are not alone. As noted before, research has consistently shown that most actively managed funds are cost-inefficient relative to comparable index funds.

The purpose of this post was to alert investors, in both private and 4091(k)/403(b) investment accounts, as to this issue of cost-inefficiency and to inform them about the simple tool, the Active Management Value RatioTM 3.0 that is available for that can be used to calculate the cost-efficiency of actively managed mutual funds.

For benchmarking purposes, I typically use Vanguard’s and/or Fidelity’s low-cost index funds. The returns and costs for both funds are essentially the same, so the AMVR results are usually similar as well. The cost and return data is available on at sites such as morningstar.com, marketwatch.com, and yahoo.finance.com.

Going Forward

In closing, the Active Management Value RatioTM is based upon the research of investment icons such as Charles D. Ellis, Nobel laureate William F. Sharpe, and Burton M. Malkiel. In analyzing an investment option, Nobel laureate William F. Sharpe has stated that

‘[t]he best way to measure a manager’s performance is to compare his or her return with that of a comparable passive alternative.’ 5

Building on Sharpe’s theory, Ellis has provided further advice on the process used in evaluating the cost-efficiency of an actively managed mutual fund.

So, the incremental fees for an actively managed mutual fund relative to its incremental returns should always be compared to the fees for a comparable index fund relative to its returns. When you do this, you’ll quickly see that that the incremental fees for active management are really, really high—on average, over 100% of incremental returns!6

As noted ERISA attorney Fred Reish likes to say, “forewarned is forearmed.”

Notes

1. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010).

2.. Charles D. Ellis, The Death of Active Investing, Financial Times,January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e.

3. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016.

4. Mark Carhart, On Persistence in Mutual Fund Performance, Journal of Finance, Vol. 52, No. 1, 57-8 (1997).

5. William F. Sharpe, “The Arithmetic of Active Investing,” available online at https://web.stanford.edu/~wfsharpe/art/active/active.htm.

6. Charles D. Ellis, “Letter to the Grandkids: 12 Essential Investing Guidelines,” available online athttps://www.forbes.com/sites/investor/2014/03/13/letter-to-the-grandkids-12-essential-investing-guidelines/#cd420613736c

© Copyright 2021 InvestSense, LLC. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.