“Make as much money as you can and keep what you get. That’s the way to become rich.” – Scottish adage

When I tell people that I am a wealth preservation attorney, I often get the obligatory inquisitive look, followed by “what’s that” question. In my law practice, wealth preservation law covers several areas of the law, primarily wealth management, tax planning, estate planning, and asset protection. The primary focus is to address each of these areas, analyze a client’s current situation, and reduce or eliminate any unnecessary exposure to actual or potential losses

Many people mistakenly believe that wealth preservation is only for high net worth individuals who needs trusts and other expensive asset protection tools and strategies. In truth, the most effective and easiest wealth preservation strategy is to effectively diversify all investment accounts, including 401(k) accounts and IRAs, and avoid unnecessary costs by only selecting cost-efficient investments.

With regard to wealth management, I analyze a clients’ current investment portfolio in overall suitability and efficiency, in terms of both cost and risk management. I draw heavily on over thirty years of experience in the area of quality of financial advice, including various stints as a compliance director. both for general securities and investment adviser operations.

I use three proprietary metrics, – the Active Management Value Ratio™ 3.0, the Fiduciary Prudence Score, and a proprietary stress test. Relying on these metrics, we often find situations where clients are paying fees that are often 300-400 percent, or more, higher than necessary to get similar, or better, performance from comparable, less expensive investment options.

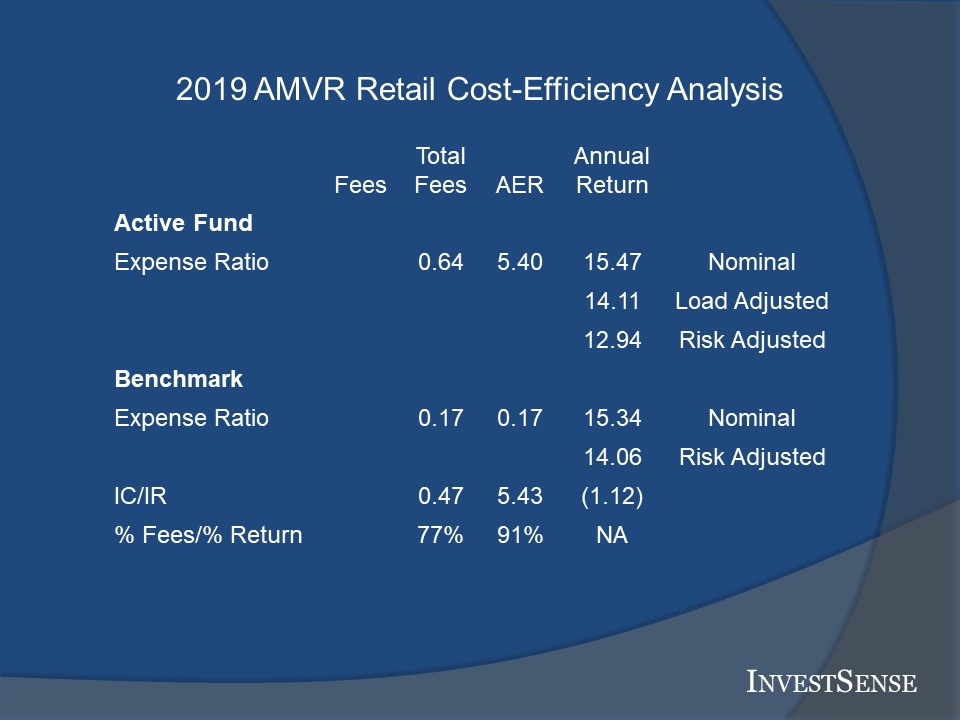

At first glance, the slide may appear confusing. However, the reader only has to answer two simple questions to understand the chart:

- Did the actively managed fund provide a positive incremental return, i.e., did the actively managed fund outperform the benchmark/index fund?

- If so, did the actively managed fund’s incremental return exceed the fund’s incremental costs, i.e., was the actively managed fund cost-efficient.

If the answer to either of the two questions is “no,” then the actively managed fund is not cost-efficient, and therefor is not a prudent investment choice.

In this example, the answer to both questions is “no.” In this example, the data is expressed in terms of basis points, an industry term. A basis point is equal to 1/100 of one percent (.01). Non-financial professionals often say it is easier to “monetize” the AMVR analyses, tothink of basis points in terms of dollar, even though that is not technically correct.

In this case, “monetizing” the analysis, an investor could pay $17 and obtain an annualized return of 14.06 percent, or pay $47 dollars and receive no additional benefit over and above that of the benchmark. In fact, the investor in the actively managed fund would actually be paying to incur a loss due to the actively managed fund’s relative under-performance.

Note the “Load Adjusted” note in the annualized return column for the active fund. Actively managed funds usually imposes a “front-end” load, or commission, at the time that an investor purchases shares in their fund. The “front-end load is often in the range of 6-6.5 percent. The front-end load is immediately deducted from the amount of the investor’s investment. This not only reduces the actual amount of the investor’s investment, but also the investor’s end-return relative to funds that do not impose front-end loads.

Note: Funds in retirement plans such as 401(k) and 403(b) plans should never charge charge loads. IRA investors should never pay front-end loads either and reject any funds that attempt to do so.

I also analyze a client’s investment and financial situation in terms of the client’s overall financial needs and plans. As an example, variable annuities can basically destroy a client’s estate plan is the client annuitizes the annuity prior to his/her death by removing the asset from the estate plan. A variable annuity can also have serious implications for those who need Medicaid later in life. These are all issues which should really be considered prior to investing, but definitely analyzed at some point in case steps should be considered to minimize any potential damage.

Tax planning is an obvious part of wealth management. As legendary jurist Judge Learned Hand stated, there is nothing wrong or illegal with arranging one’s affairs so as to minimize taxes. Losses due to taxes obviously reduce wealth and can significantly reduce one’s estate. Tax laws can impact investment choices, e.g., Traditional IRAs vs Roth IRAs, tax deferred investments options vs. non-tax deferred investment options. Tax laws can impact estate plans e.g., estate equalization strategies, marital property considerations, disclaimer strategies. With the constant change in tax laws, it is critical that clients utilize all possible resources, including tax attorneys and CPAs, in order to keep their comprehensive wealth management up-to-date with regard to tax planning.

Estate planning focuses on the efficient distribution of one’s estate. Efficient distribution focuses on both ensuring that the deceased’s last wishes are honored, but also that the estate is not greatly reduced due to the impact of taxes. We will discuss estate planning more in next week’s post on distribution. For now, let’s just say that there are a number of strategies, including estate equalization, trusts and qualified disclaimers that can be used as part of an effective wealth management process.

Finally, studies consistently show that the public wants to know about asset protection strategies, particularly the use of asset protection trusts. There are basically two types of asset protection trust – domestic asset protection trust (DAPTs) and foreign asset protection trusts (FAPTs). The most popular domestic jurisdictions are currently Nevada, Delaware, Alaska and South Dakota. Popular foreign jurisdictions include the Cook Islands, Nevis, Isle of Man and the Cayman Islands.

In choosing a jurisdiction for an asset protection trust, there are several things to consider. First and foremost, the asset protection laws differ from jurisdiction to jurisdiction. Two of the most important legal issues to consider are the statute of limitations (SLs)/contestability provisions and the exceptions from protection. The optimum situation is a jurisdiction with short SL/contestability period and as few exceptions as possible. With DAPTs, there is also the issue of whether the DAPT state will honor and enforce a judgement from another state under the “full faith and credit” provision of the U.S. Constitution.

I have a lot of people contact me and say they are going to be sued, so they need an asset protection trust…now! Then I explain a couple of things of things about asset protection trusts, such as (1) asset protection trusts cannot be used to perpetuate fraud; (2) the earlier an asset protection trust is created, the greater the protection; and (3) the effectiveness of an asset protection trust is inversely related to the amount of rights and powers retained by the trust’s grantor. In many cases, it is too late to create an effective asset protection trust, as the event creating the liability has already occurred.

The key to effective wealth preservation is not to view wealth preservation in isolation, but rather as part of a comprehensive wealth management plan. Wealth preservation involves various aspects of the law, including wealth management, tax planning, estate planning, retirement distribution planning and asset protection. The key is to also create a strong team of professionals experienced in these areas and work towards the client’s goals and needs.

© 2013-2021 InvestSense, LLC. All rights reserved.

This article is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.