During his term as Chairman of the Securities and Exchange Commission (SEC).(1993-2001), Arthur Levitt focused more on investor protection than perhaps any other recent SEC Chairman. His advice from a 1999 speech, “Financial Self-Defense: Tips From and SEC Insider,” is still relevant and valuable to investors today.

There are more ways to invest than ever before. But there also seem to be more ways to be confused – or to be misled.

America’s marketplace is generally honest – but there are some crooks out there. And, there’s only so much that law enforcement and regulatory watchdog agencies, like the SEC, can do.

You’ve got to do your part, too….You also need to be on guard when dealing with investment professionals. The vast majority of people selling securities are honest. But we do have people who walk a fine line between good sales practices and poor sales practice….

An informed investor looks beyond the packaging of a product and also sees what’s inside.1

Sadly, recently the SEC has seemingly focused more on protecting the interests of Wall Street rather than on the protection of investors, one of the stated purposes and goals of the commission. As a result, Chairman Levitt’s admonition to assume greater responsibility for self-protection when dealing with the investment and/or the pension/retirement industries is equally applicable today.

Active versus Passive-Costs Matter

The late John Bogle, founder of the Vanguard Group, was fond of reminding investors that “costs matter.” In the ongoing debate over actively managed funds compared to passively managed index funds, one issue that is undeniable is that actively managed mutual funds, by their very nature, will have higher costs than index funds, specifically trading and management costs.

Advocates of actively managed funds argue that that the higher costs are justified by the fact that actively managed funds produce higher returns for investors. Evidence would suggest otherwise. So the questions are (1) how much higher costs does an actively managed fund have compared to a comparable benchmark index fund, and (2) what impact do the higher costs have on a fund’s performance?

As for a fund’s management fees, those are reflected in a fund’s annual expense ratio/fee. Whether those fees are justified or not are reflected in the fund’s performance relative to a comparable benchmark index fund, as well as the actual amount of active management actually provided by a fund.

As for trading costs, mutual funds are not currently required to provide their actual trading costs to investors. Instead, funds are allowed to group actual trading costs into a generic category of “operating costs,” which are then deducted from a fund’s gross return in reporting a fund’s performance.

Allowing an actively managed fund to “hide” such important information as trading costs prevents investors from being able to compare such costs to make a meaningful evaluation of a fund’s efficiency in managing the fund. As the SEC and other government agencies have noted, such costs do have a significant impact on an investor’s return. Each additional 1 percent in fees and costs reduces an investor’s end return by approximately 17-18 percent over a twenty year period.

Fortunately, Bogle recognized the importance of trading costs. He created a simple metric that allows investors to create a proxy for such cost and compare such costs between funds. Bogle’s metric simply doubles a fund’s reported annual turnover ratio and multiples that number by 0.60. So, if a fund has an annual turnover ratio of 50 percent, Bogle’s metric would result in an estimated trading cost of .0.60 for comparison purposes.

Bogle himself acknowledged that his metric probably understates a fund’s actual trading costs. However, the metric is still valuable in that it provides investors, fiduciaries and attorneys with a means of comparing such costs. As studies and simple mathematics show, the potential impact of such costs is simply too important to ignore.

Investor Self-Defense and the Active Management Value Ratio™

Unfortunately, the sheer number of investment options and the complexity of same make it extremely difficult for investors to independently evaluate the available investment options. Inexplicably, despite the acknowledged importance of pension/retirement plans, such as 401(k) and 403(b) plans, and “retirement readiness,” there is no express requirement that employers provide employees with any type of investment education.

Fortunately, there are simple and extremely effective tools and strategies that investors and pension plan participants can use to independently evaluate investment options. One such tool is a metric I created, the Active Management Value Ratio™ (AMVR). The AMVR allows investors and others to follow Chairman Levitt’s advice and look “beyond the packaging of a product and also sees what’s inside.” The AMVR allows investors, plan participants, fiduciaries and attorneys to evaluate the cost-efficiency of an actively managed mutual fund.

The Supreme Court has stated that the Restatement of Trusts (Restatement) is a key resource in interpreting fiduciary law and resolving questions regarding prudent investing. Fiduciary law requires that a fiduciary always act in the best interests of the beneficiaries and/or other parties whose interests they represent. Even when a fiduciary is not actually involved, the investment standards established by the Restatement ensure that an investor’s best interests are being served.

The AMVR incorporates the Restatement’s prudent investment standards and is simply the basic cost-benefit equation that every economics student learns in their Econ 101 class. The only difference is that the AMVR compares the incremental costs and incremental returns between an actively managed mutual fund and a comparable index fund. Applying simple common sense, actively managed funds whose incremental costs exceed the fund’s incremental returns are deemed to be cost-inefficient, and thus an imprudent investment.

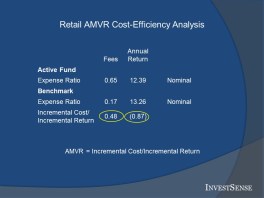

A simple worksheet would be as follows:

In the worksheet above, assume that we are comparing an actively managed mutual fund and a comparable index fund with the following cost and return data:

Active Fund: Annual Expense Ratio 1.00%/5-Year Annualized Return 10.50%

Index Fund: Annual Expense Ratio .0.10%/5-Year Annualized Return 10.00%

As a result, the actively managed fund would have incremental costs of 90 basis points and incremental returns of only 50 basis points. (A basis point is equal to .01 percent.) A fund’s AMVR score is simply its incremental costs divided by the fund’s incremental returns.

Here, the actively managed fund’s AMVR score would be 1.80 (.90/.50). An AMVR score greater than 1.00 indicates that a fund’s incremental costs are greater than its incremental returns, indicating that the fund is not cost-efficient. An AMVR less than zero indicates that the actively managed fund underperformed its benchmark, providing no positive return for an investor.

In interpreting the AMVR, an investor or other user only needs to answer two questions:

- Did the fund being evaluated provide a positive incremental return?

- If so, did the fund’s incremental return exceed the fund’s incremental costs?

If the answer to either of these questions is “no,” the fund does not qualify as a prudent investment under the prudent investment standards established by the Restatement.

The AMVR calculation process provides another important piece of information regarding the cost-efficiency of an actively managed fund. In the example above, the numbers show that 90 percent of the actively managed fund’s total fee is only producing approximately 5 percent of the fund’s return. This is yet another example of the fund’s cost-inefficiency and further proof that it would not be a prudent investment choice.

Investor Protection Plus

While the AMVR example provided demonstrates the importance of evaluating the cost-efficiency of actively managed mutual funds, the nominal, or reported, numbers may not properly factor in the actual contribution of active management in the fund’s performance, and thus may understate the implicit efficiencyof the fund’s fees and costs..Investors can avoid this oversight by simply considering an actively managed fund’s R-squared correlation number.

Morningstar states that

R-squared measures the relationship between a portfolio and its benchmark. It can be thought of as a percentage from 1 to 10.

If you want a portfolio that moves like the benchmark, you’d want a portfolio with a high R-squared. If you want a portfolio that doesn’t move at all like the benchmark, you’d want a low R-squared.

An R-squared of 100 indicates that all movements of a portfolio can be explained by movements in the benchmark. Conversely, a low R-squared indicates that very few of the portfolio’s movements can be explained by movements in its benchmark index. An R-squared measure of 35, for example, means that only 35% of the portfolio’s movements can be explained by movements in the benchmark index.

So, by reviewing an actively managed fund’s R-squared number, an investor can get an estimate of exactly how much of an actively managed fund’s performance can be attributable to the fund’s management team, as opposed to the performance of an underlying market index. In our example, the actively managed fund’s R-squared number of 95 would indicate that 95 percent of the fund’s performance can actually be attributable to the performance of the benchmark, with only 5 percent of the fund’s return being attributable to the fund’s management team. In short, a fund’s R-squared score gives investors a totally new perspective on an actively managed fund’s fees and costs, specifically the fund’s annual expense ratio/fee.

Ross Miller created a metric, the Active Expense Ratio (AER). Miller has stated that the AER measures the implicit cost of an actively managed fund’s annual expense ratio/fee by factoring in the fund’s R-squared number. The higher an actively managed fund’s R-squared correlation number, the lower the actual contribution of active management to the fund’s performance and the higher the fund’s AER score.

Using our earlier example and assuming an R-squared correlation number of 95 percent for the actively managed fund, the cost-inefficiency of the actively managed fund becomes even more apparent.

The combination of high incremental costs (90) and a high R-squared correlation number (95) result in an AER of 5.35, over 400 percent higher than the fund’s stated annual expense ratio. This further supports the argument that investors, fiduciaries and attorneys should always factor in an actively managed fund’s R-squared number.

Morningstar provides an R-squared correlation number for each of the funds it analyzes under the “Risks” tab. The only issue with Morningstar’s R-squared number is that they often use the S&P 500 index as the benchmark for all equity funds. Since Morningstar classifies S&P 500 Index funds as large-cap blend funds, the use of the index for other categories of funds is subject to questioning. At InvestSense, we calculate our own R-squared correlation numbers using comparable Vanguard index funds from the same Morningstar style box as the actively managed fund being analyzed.

While advocates of actively managed funds would argue that the results can be manipulated by assigning a high R-squared number to a fund, a simple review of data from the Morningstar Data Research Center will show that a significant percentage of U.S. domestic equity funds currently have a R-squared number of 90 or above. And yet, inexplicably, the majority of investment holdings in personal investment accounts and pension plans are still in actively managed mutual funds.

Lessons Learned

When people ask me what I do for a living, I tell them that I am a wealth preservation attorney. When they follow-up by asking me what that means, I tell them that I combine my 20+ years legal experience as a securities/RIA compliance director and estate planner with my 30+ years experience as a financial planner to help clients develop a REAL wealth management/preservation program that focuses on the accumulation, protection, and distribution of wealth.

“Get what you can, and keep what you have. That’s the way to get rich.” That Scottish adage essentially sums up my philosophy about wealth management and preservation. I have written various articles on the three aspects of REAL wealth management and preservation, all of which are available on this blog. However, as Chairman Levitt pointed out, investors need to have a better understanding of investing in order to protect their financial security.

In my practices, we provide various comprehensive forensic analyses that calculate the efficiency of an actively managed fund, in terms of both risk management and cost efficiency, as well as a fund’s consistency of performance. However, the AMVR itself provides public investors, fiduciaries and others with a simple, yet effective, means of avoiding unnecessary investment losses due to cost-inefficient actively managed mutual funds.

The issue of cost-efficient investing is gaining increased attention in both the legal and wealth management communities. Studies have consistently concluded that the overwhelming majority of actively managed mutual funds are not cost-efficient, resulting in statements such as

- 99% of actively managed funds do not beat their index fund alternatives over the long term net of fees.2

- Increasing numbers of clients will realize that in toe-to-toe competition versus near–equal competitors, most active managers will not and cannot recover the costs and fees they charge.3

- [T]here is strong evidence that the vast majority of active managers are unable to produce excess returns that cover their costs.4

- [T]he investment costs of expense ratios, transaction costs and load fees all have a direct, negative impact on performance….[The study’s findings] suggest that mutual funds, on average, do not recoup their investment costs through higher returns.5

Financial plans often recommend that a customer spend less money than they earn. The AMVR just stands for the proposition of avoiding actively managed funds that are not cost-efficient, funds whose incremental costs exceed their incremental returns.

Advocates of active management will often claim that active management allows mutual funds to cover the higher costs associated with actively managed mutual funds, namely higher annual expense ratios/fees and higher trading costs. The above-referenced studies prove otherwise. Furthermore, given the high R-squared correlation numbers of many U.S. domestic equity-based funds, it can be argued that such funds are “closet index,” or “mirror” funds, further reducing any chance that the fund’s active management can cover their extra costs

Very few investors and investment fiduciaries even consider a fund’s R-squared correlation numbers. Stockbrokers and other investment professionals try to avoid the issue due to the overwhelmingly negative evidence on the performance on the commission-based actively managed funds they sell,

Nevertheless, in addition to the two AMVR questions we previously mentioned, we suggest that all investors and investment fiduciaries doing business with stockbrokers and/or other financial salesmen always include the following two questions as part of their self-defense strategy:

- Will you be acting as a fiduciary in advising me/managing my account, with full disclosure of material facts and putting my best interests first?

- Will all of the investments you recommend be cost-efficient, with incremental returns exceeding the investment’s incremental cost relative to an appropriate benchmark?

And finally, if the stockbroker or financial adviser answers “yes“ to both questions, ask them if they are willing to put those assurances in writing. One of the first things every law student learns in their first-year contracts class is that a verbal promise is only as good as the paper it is written on.

Notes

1. https://www.sec.gov/news/speech/speecharchive/1999/spch305.htm

2. Laurent Barras, Olivier Scaillet and Russ Wermers, False Discoveries in Mutual Fund Performance: Measuring Luck in Estimated Alphas, 65 J. FINANCE 179, 181 (2010).

3. Charles D. Ellis, The Death of Active Investing, Financial Times,January 20, 2017, available online at https://www.ft.com/content/6b2d5490-d9bb-11e6-944b-eb37a6aa8e.

4. Philip Meyer-Braun, Mutual Fund Performance Through a Five-Factor Lens, Dimensional Fund Advisors, L.P., August 2016.

5. Mark Carhart, On Persistence in Mutual Fund Performance, 52 J. FINANCE, 52, 57-8 (1997).

© Copyright 2019 The Watkins Law Firm/InvestSense. All rights reserved.

This article is for informational purposes only, and is neither designed nor intended to provide legal, investment, or other professional advice since such advice always requires consideration of individual circumstances. If legal, investment, or other professional assistance is needed, the services of an attorney or other professional advisor should be sought.